AT&T (T) — Risk-Impact & Scenario-Based Analysis (2025 Outlook)

Overview (short)

AT&T is one of the largest integrated communications companies in the U.S., operating across wireless (mobility), broadband (AT&T Fiber), and business wireline services. After exiting most media ownership and doubling down on 5G and fiber, AT&T’s 2025 story is now focused on subscriber growth, margin recovery, heavy but disciplined capital investment, debt reduction and cash returns to shareholders. Recent quarterly reporting and company guidance show the firm reiterating a multi-year plan that leans on converged wireless+fiber economics — but it still faces legacy debt and execution risks. about.att.com+1

2025 outlook at a glance (key metrics)

| Metric / Item | Recent reading (2025) | What it implies |

|---|---|---|

| Consolidated service revenue guidance | Growth in low single-digits (company guidance). about.att.com | Organic service revenue expansion — not explosive, but growth driven by mobility and fiber. |

| Mobility service revenue | Growth ~3% or better (guidance). about.att.com | Wireless remains the cash engine. |

| Consumer fiber broadband revenue | Mid-to-high-teens growth (YoY) reported. investors.att.com | Fiber is the most attractive growth and margin lever. |

| Adjusted EBITDA guidance | ~3% (company targets). about.att.com | Management expects margin expansion from mix and efficiencies. |

| Capital investment (CapEx) | $22.0–$22.5 billion for 2025 (guidance). about.att.com | High investment for 5G & fiber — constrains near-term free cash flow but is strategic. |

| Long-term debt (Sept 30, 2025) | ~$123B long-term debt (latest reported). Macrotrends | Leverage remains the central balance-sheet risk to monitor. |

| Recent quarterly revenue & subscriber trends | Revenue ~$30.7B (Q3-2025); 405K postpaid phone net adds (Q3). investors.att.com+1 | Subscriber gains validate the converged strategy but business wireline weakness continues. |

(Sources: AT&T investor releases and Q3 2025 materials; debt figures from public financial data.) about.att.com+2investors.att.com+2

Primary risks and how they transmit to business outcomes

Below are the major risks for AT&T in 2025 and the primary channels by which they could impact results.

1. Leverage & interest burden (Balance-sheet risk)

Why it matters: AT&T carries very large long-term debt from past M&A and network investment cycles. While management is pursuing debt reduction and cash generation targets, high absolute debt makes AT&T vulnerable to slower free cash flow, higher rates, or credit-market shocks. Macrotrends

Impact channel: Interest expense pressure, reduced flexibility for buybacks/dividends, increased refinancing risk. If cash flow stumbles, AT&T may need to slow buybacks or re-profile capital allocation.

2. Capital allocation trade-offs (CapEx vs. cash returns)

Why it matters: AT&T needs to invest heavily in fiber and 5G (CapEx ~$22B in 2025) while simultaneously returning capital to shareholders. The timing and effectiveness of these investments determine future revenue growth and free cash flow trajectories. about.att.com

Impact channel: Too little investment risks slower subscriber growth and competitive loss; too much constrains dividends/share repurchases.

3. Execution risk on fiber & convergence strategy

Why it matters: The strategy of bundling wireless + fiber (“convergence”) is working — fiber revenue is growing at double digits and converged ARPU is attractive — but scaling fiber to millions of passings is operationally intensive and competitive. Subscriber economics must remain favorable. investors.att.com

Impact channel: Missed fiber rollouts or weak take rates reduce projected revenue and free cash flow improvements.

4. Competition and pricing pressure (market risk)

Why it matters: Verizon, T-Mobile and regional ISPs compete aggressively on price, promotions and new services. Wireless market saturation in some cohorts and price competition for unlimited plans can compress margins. CRN

Impact channel: Lower ARPU, higher churn, elevated customer-acquisition costs.

5. Business wireline decline & enterprise transformation risk

Why it matters: Business wireline revenue continues to decline as enterprises migrate away from legacy services. AT&T must execute transformation and grow higher value-added enterprise and managed services. investors.att.com

Impact channel: Revenue base erosion on the business side could offset consumer gains if not replaced.

6. Regulatory, geopolitical or cyber risks

Why it matters: Telecom is regulated and reliant on spectrum policy, security requirements, and supply-chain continuity. Cyber incidents can cause service outages and reputational harm.

Impact channel: Fines, remediation costs, temporary subscriber attrition or investment delays.

Risk-Impact Matrix (compact)

| Risk | Likelihood (near-term) | Severity (impact) | Primary metric to watch |

|---|---|---|---|

| Leverage / debt | Medium | High | Net debt / Adj. EBITDA |

| CapEx vs cash returns | High | Medium-High | Free cash flow; CapEx run-rate |

| Fiber execution | Medium | High | Fiber passings, net adds, ARPU |

| Wireless competition | High | Medium | Mobility service revenue growth |

| Business wireline decline | High | Medium | Business wireline revenue YoY |

| Regulatory / cyber | Low-Medium | High | Regulatory filings / incident reports |

Scenario-based outlook for 2025

Below are three practical scenarios that capture plausible outcomes for AT&T in 2025, tying risks to measurable impacts.

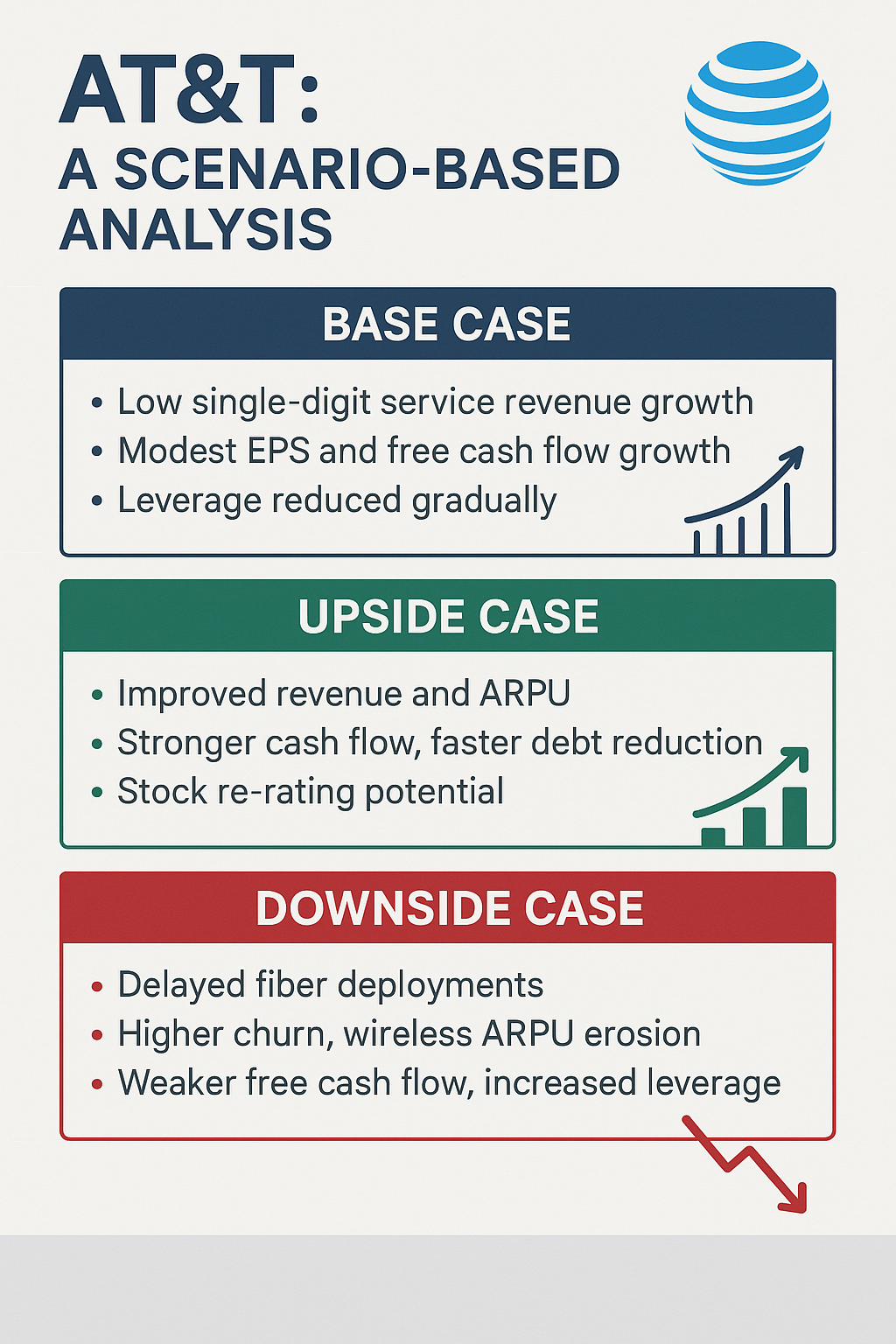

Base Case (management guide)

Assumptions: AT&T executes on fiber rollouts and continues steady postpaid phone growth; mobility service revenues grow ~3%; adjusted EBITDA expands ~3%; CapEx remains ~$22–22.5B; debt reduction progresses modestly. about.att.com+1

Outcomes: Consolidated service revenue grows low single-digits; fiber revenue grows mid-to-high teens; adjusted EPS and free cash flow improve modestly, enabling continued dividends and targeted buybacks. Credit metrics slowly improve; leverage remains elevated but manageable. This is the company’s stated path. about.att.com

Upside Case (execution + a benign macro)

Assumptions: Fiber take-rates exceed plan, converged customer gains accelerate, wireless ARPU rises, and business wireline deterioration is offset by new enterprise products. Also, modest non-recurring gains or asset monetizations accelerate debt paydown.

Outcomes: Faster debt reduction, stronger free cash flow (>guidance), more aggressive buybacks and higher investor multiple. AT&T becomes viewed as growth-plus-income stock rather than balance-sheet risk. Market re-rating possible.

Downside Case (execution / macro hit)

Assumptions: Fiber deployments face delays or cost overruns; wireless pricing war forces ARPU decline; interest rates rise or refinancing windows tighten; business wireline erosion persists.

Outcomes: Free cash flow falls short, leverage metrics worsen, management pauses buybacks or cuts discretionary returns, and credit concerns resurface. Share price weakens and strategic options (asset sales or deeper restructuring) may arise.

Key indicators to watch (short checklist)

-

Net debt / adjusted EBITDA ratio — single best indicator of balance-sheet health. Macrotrends

-

AT&T Fiber passings & net adds — growth here underpins revenue and margin improvement. investors.att.com

-

Mobility service revenue growth / postpaid ARPU — shows pricing power and subscriber quality. investors.att.com

-

CapEx run-rate vs. guidance — overspend or underspend has strategic consequences. about.att.com

-

Free cash flow & management commentary on capital returns — indicates willingness to shrink debt or reward shareholders. Reuters

Strategic implications — management & investors

For management:

-

Continue to prioritize high-return fiber buildouts and bundled offers that increase ARPU and reduce churn.

-

Keep a disciplined approach to capital allocation: balance necessary CapEx with credible debt reduction milestones to preserve financial optionality.

-

Communicate transparently on progress (passings, take rates, cost per install) — investors reward clear, measurable operational delivery.

For investors:

-

AT&T is today a hybrid value-income play with optionality on convergence. If you value stable dividends plus upside from execution, AT&T is compelling only if you are comfortable with material leverage and monitor the debt trajectory closely. Macrotrends

-

Risk-tolerant investors should track subscriber and free cash flow inflection points; conservative investors may prefer exposure only once leverage moves into a more comfortable band or buybacks resume meaningfully.

Final summary — where AT&T stands in 2025

AT&T’s 2025 outlook is a juxtaposition of strong operational momentum in mobility and fiber (which the company is explicitly guiding to continue) with enduring balance-sheet baggage from past strategic decisions. Management’s current thesis — invest aggressively in 5G and fiber, grow converged customers, then use improving cash flow to reduce debt and return capital — is plausible and supported by early subscriber metrics and reiterated guidance. But the plan is execution-dependent, and the single largest downside risk remains balance-sheet/interest-rate stress if free cash flow underperforms. about.att.com+2investors.att.com+2